Career

Recently accepted positions

Recent Kellogg graduates accepted positions in:

Corporate Social Responsibility

at Facebook, General Electric, Starbucks, and more

Public/Government

at the White House, RTI International, National Park Service, New York Public Radio, and more

International Development

at Joseph Project, United Nations, and Fish4Hope, and more

Social Enterprise

at Subway Kenya, Inspirotec, Piece & Company, Koa Organic Beverages, and Story2 LLC., and more

Kellogg prepares students and alumni to be change-makers for today’s most pressing challenges worldwide. Career supports are abundant and help students and alumni seeking to foster social impact across diverse sectors and roles.

Whether in full-time social impact work, focusing on sustainability and impact through a corporate lens, or in dedication to board service, philanthropy or public service, Kellogg students and alumni succeed in securing roles that forge impact.

Kellogg connects students and alumni to a rich portfolio of employers and opportunities for careers and internships. With employers visiting campus, hosting interviews and meet-and-greet sessions, Kellogg students gain the exposure to a broad range of employers and possibilities in the impact space.

Career Support

Kellogg prepares students for success in business, and our world-renowned Career Management Center equips them to manage and foster social impact in their careers over a lifetime. With career coaches who are experts on impact career tracks to on-campus interviewing and career visits from impact companies and organizations, to a comprehensive job board with opportunities across impact sectors, Kellogg’s Career Management Center and social impact professors and team support students and alumni to forge their own paths in their impact careers.

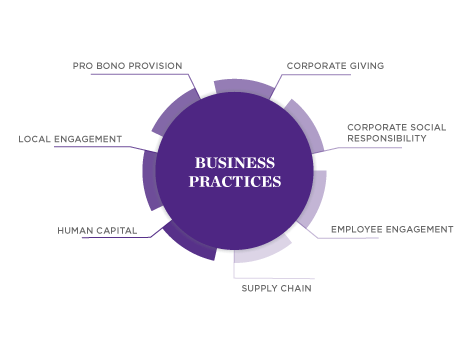

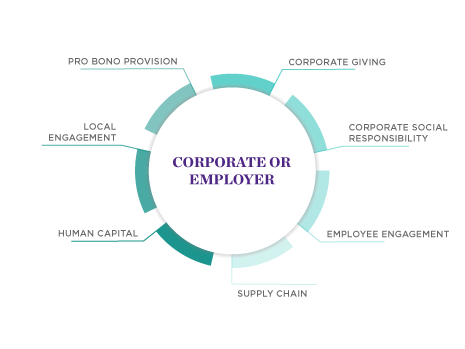

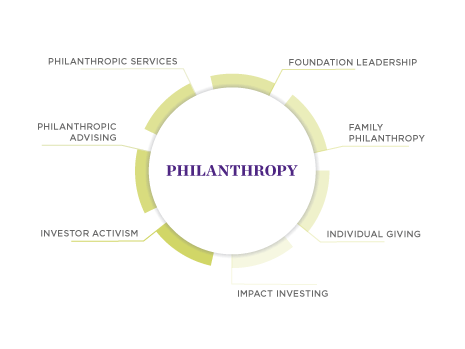

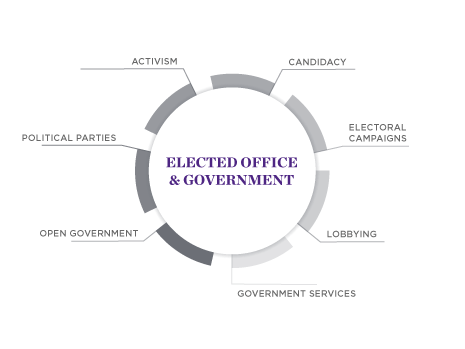

Impact careers: Jumping in with both feet

Corporate or Employer

Philanthropy

Elected Office and Government

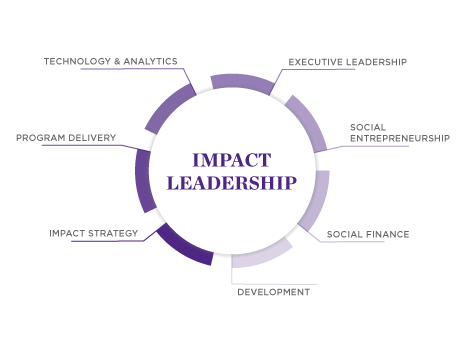

Impact Leadership

Using your skills and resources: ways to be involved

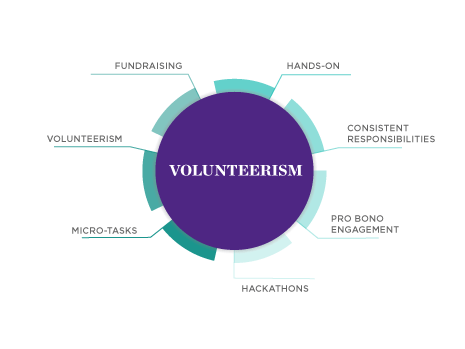

Volunteerism

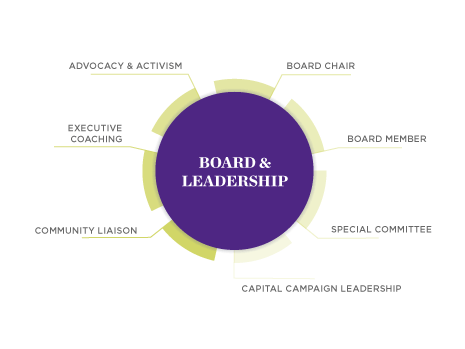

Board and Leadership

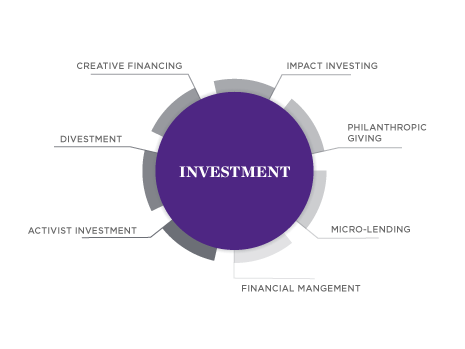

Investment