|

|||||

|

|

|

|||||

|

|

|

|||||||||||||||||||

Knowing that at the time the spread over the agency’s 20-year optionless rate should have been around 60 basis points, I was astonished to find that the proposed coupon premium was a mere 25 basis points. It seemed too good to be true. On closer inspection, however, I discovered that the deal had some unusual elements. The underwriting fee, at 2.30 percent of the principal, was much higher than the 0.50 percent usually paid by the agency for a 20-year deal. And it contained an “estate put,” a term I had never even heard of before. Having to model the estate put was an unexpected challenge. My expertise being largely honed in the institutional arena, I was now entering the world of retail bonds. What is an Estate Put?

Old-timers will likely recall the Estate Tax Anticipation Bonds sold by the U.S. Treasury. Known colloquially as “flower bonds,” they had the novel feature that, regardless of their market value, the IRS would accept them at par if used to pay the estate taxes of a deceased holder. Elderly investors, for whom these bonds were designed, were willing to pay up for them even though their coupons were below the prevailing market rate. The last flower bonds matured in 1998 – the lucky holders who outlived them must have been delighted to lose the bet.

I discovered flower bonds quite by accident, while I was attempting to reverse engineer a mysterious transaction reported in the financial press. The transaction entailed what I believe was the first OID (original issue discount) bond. Eventually, it became apparent that a pension fund basically wanted to get some flower bonds off its books without having to record a loss. Why a pension fund would purchase flower bonds in the first place is a mystery in itself (see “Innovations in Corporate Finance: Deep Discount Private Placements” in Financial Management, Spring 1982).

The estate put is a variation on the flower bond concept. Bonds with this feature – also known as “survivor’s option” or less euphemistically, “death put” – can be redeemed by the estate at par in the event of the demise of the holder. The issuer imposes an annual ceiling on the face amount of bonds it accepts in aggregate (one or two percent of issue size). There is also a limitation per estate, ranging from about $25,000 to $250,000.

The estate put feature is designed strictly for retail investors – obviously, it has no value to institutions. It is common in both taxable and tax-exempt bonds, and lately, in certificates of deposit, where no annual ceilings apply. Since CDs generally have a shorter maturity relative to bonds, the estate put is less valuable.

The Retail Bond Market

Mom and Pop investors put a premium on cash flow and capital preservation, so retail bonds pay more frequently (monthly or quarterly) than regular bonds and are often insured if not already rated AAA. An intriguing aspect of bond insurance in the tax-exempt market is that lower rated issuers, apart from gaining access to AAA investors, save markedly more from the lower (insured) coupon than they pay in insurance costs.

By their nature, retail deals involve selling bonds in small lots to individual investors. Thus a $50 million deal might be sold in numerous individual transactions whose size may be just a few thousand dollars. The sales commission per transaction adds up, making retail distribution a costly process. In contrast, an institutional deal of, say, $250 million may be picked up in full by a handful of money managers.

Today there are several programs that specialize in selling bonds to retail investors. We have already mentioned Edward Jones, which has thousands of one-man offices nationwide. Another is LaSalle Bank, a subsidiary of ABN AMRO, which runs its Direct Access Notes SM program for taxable bonds of frequent issuers, such as Freddie Mac, TVA and John Hancock. Bank of America runs a competing InterNotes SM program. The aggregate outstanding volume of bonds designed primarily for retail is in the hundreds of billions of dollars.

Secondary market trading is obviously modest, since the inventory is distributed among buy-and-hold investors. If an individual investor decides to sell, the bonds are unlikely to find their way back to the retail market. For this reason secondary market prices tend to be depressed. Uninsured retail bonds of fallen angels trade particularly poorly.

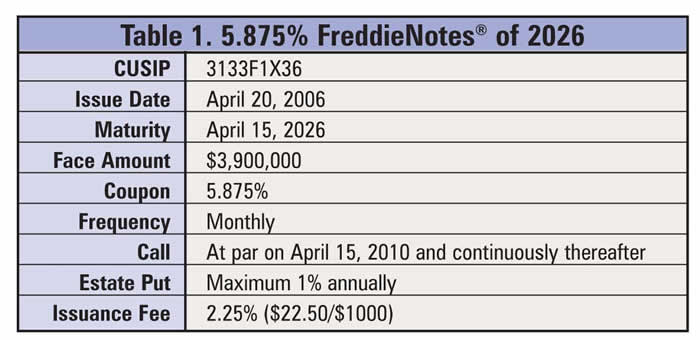

Let’s look at a recent FreddieNote® issued through the DANs program.

Note the short lockout, the initial call at par, the estate put, the high issuance fee (for an institutional deal of this maturity, 0.50 percent would be typical), the monthly interest and the tiny size (in contrast, Freddie Mac’s Reference Notes® are issued in sizes of several billion dollars).

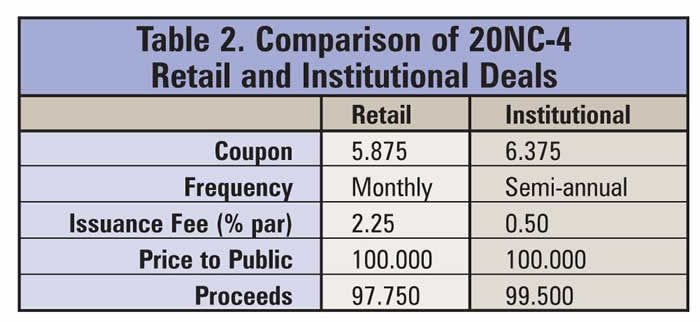

So why would Freddie Mac bother issuing these notes? Undoubtedly because the price was right – they must have been attractive relative to institutional alternatives. But how should an issuer compare retail and institutional deals (of similar maturity and duration) on an apples-to-apples basis? We advise issuers to base their decision on expected cost per dollar raised. Modeling the OptionsThe calculation of expected cost should account for both the issuer’s call and the investor’s estate put options. The two are interrelated, because the exercise of one precludes the exercise of the other. Let’s explore how they should be modeled. First, consider the estate put. The bonds should be put only if they are worth less than par; otherwise it is preferable to retain or sell them. Therefore the issuer should not treat the estate put as an amortization of principal. Assuming that a certain percentage of the issue would be put annually independent of interest rates would lead to a grave underestimation of the cost of the estate put. From the issuer’s perspective the contractually specified annual maximum is the worst-case scenario. If experience or perception indicates that only some fraction of the maximum is likely to be put (based on mortality expectations), this lower estimate may be used. Let’s turn to the call option. The issuer should call and refund when rates are sufficiently low. The methodology for determining the optimum time to call is familiar to fixed income quants. But here, there is an added subtlety: Apart from lowering interest expense, calling also eliminates future puts. Determining the True Cost of BorrowingIf we compare the offering circular of a retail deal to the “tombstone” of an institutional one, the differences are striking (see Table 2). How should the issuer make the right choice? In our advisory work, we developed what I believe is the appropriate yardstick – expected cost per dollar raised. The deal with the lowest such measure wins. If the issuer is a tax-paying entity, the calculation should be done on an after-tax basis (although, for simplicity, I omit this consideration from the example here).

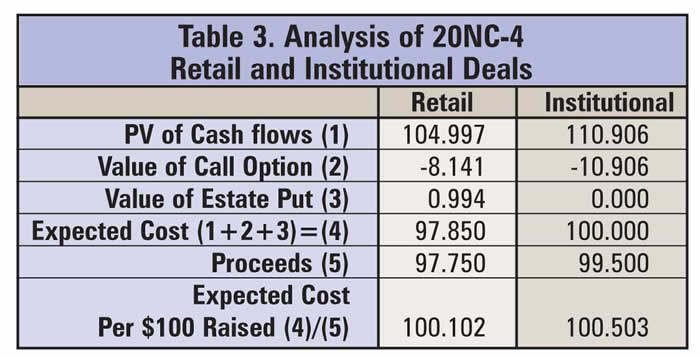

The required market inputs are the issuer’s optionless yield curve and the appropriate interest rate volatility (and the issuer’s marginal tax rate, if relevant). Table 3 shows the results of the analysis for a 20-year bond callable after four years (20NC-4) in the retail and institutional markets. The expected cost per $100 raised is lower for the retail issue ($100.102) than for the institutional deal ($100.503). In general, because an institutional deal is fairly priced (professional investors presumably would not overpay), its expected cost will exceed the proceeds.

As mentioned above, the indenture limits the amount of annual puts to some small percentage of the principal, say two percent. Under the worst-case scenario, this is the maximum amount that must be accepted. But if the issuer considers it unlikely that the mortality rate of the investors will reach this contractual maximum, a lower rate, say 1.25 percent, may be used. Clearly the lower the expected mortality rate, the lower is the expected cost.

Investor’s Perspective

In contrast with the issuer, for an investor, the value of a bond with an estate put depends on a single actuarial table – his own. Naturally, the put feature is much more valuable to an elderly person than it would be in the custodial account of a minor. I mentioned an analogous consideration above, in the context of flower bonds.

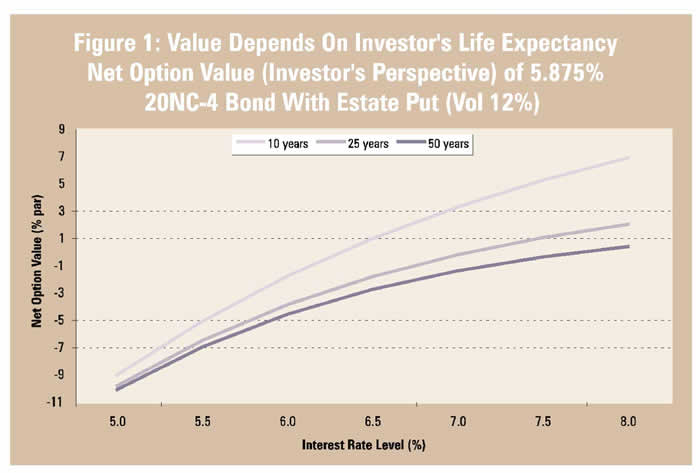

Figure 1 shows how the net option value of our featured 20-year 5 7/8 percent retail bond depends on the investor’s mortality rate. Recall that there are two interrelated embedded options – the issuer’s call and the investor’s estate put. As one would expect, the mortality effect becomes pronounced as interest rates rise. For example, for an investor with a ten-year life expectancy, the net option value is worth 3.20 percent of principal when rates are at seven percent. When rates are low the issuer’s call option dominates, and therefore the investor’s life expectancy has a much weaker effect.

Final Thoughts

Are retail bonds a good value for issuers? The growth in volume would appear to strongly corroborate the affirmative. The lower coupon is attractive relative to the institutional markets but the piecemeal nature of the distribution results in high issuance cost. And then there’s the estate put which allows the heirs of a deceased holder to redeem the bonds at par. Issuers should employ the appropriate technology to determine lowest expected cost per dollar raised when choosing between retail and institutional issues.

The appeal to retail investors comes from frequent coupon payments, security of the principal and the estate put. Should investors be buying these bonds? Apart from the appropriateness of the purchase price, the decision depends on the individual’s own life expectancy. The shorter the expected life, the more valuable is the estate put. In this context, and given the poor liquidity in the secondary market, these bonds are often worth more “dead” than “alive.” About the Author Andrew Kalotay is president of Andrew Kalotay Associates, Inc., a New York-based debt management advisory and fixed income analytics firm. He can be reached at akalotay@fenews.com. |

Measuring Market Risk, 2nd Edition |

Modeling Derivatives Applications |

Seven Signs of Ethical Collapse |

A

few years ago a federal agency asked me to review a funding proposal

from the St. Louis-based investment bank, Edward Jones. It was for a

20-year bond callable at par after four years. FEN readers

will no doubt appreciate that the call option does not come free. The

coupon premium depends on factors such as the lockout period, maturity,

the prevailing yield curve and interest rate volatility. With the

appropriate market inputs, it can be backed into using standard (OAS)

valuation technology.

A

few years ago a federal agency asked me to review a funding proposal

from the St. Louis-based investment bank, Edward Jones. It was for a

20-year bond callable at par after four years. FEN readers

will no doubt appreciate that the call option does not come free. The

coupon premium depends on factors such as the lockout period, maturity,

the prevailing yield curve and interest rate volatility. With the

appropriate market inputs, it can be backed into using standard (OAS)

valuation technology.